Medicare's GLP-1 Bridge Program: Weight Loss Medications for $50 Per Month A new pilot program from the Centers for Medicare & Medicaid Services (CMS) may allow eligible Medicare beneficiaries to access certain GLP-1 weight loss medications for just $50 per month through December 31, 2027. For more information about Medicare prescription drug coverage, visit Medicare Part D Information . While you must be enrolled in a Medicare Part D prescription drug plan to qualify, the GLP-1 Bridge Program operates separately from your Part D coverage. Because of this, the $50 monthly copay does not count toward your Part D deductible or annual out-of-pocket costs. Who May Qualify? The GLP-1 Bridge Program is intended for Medicare beneficiaries who need weight management treatment but do not have coverage for GLP-1 medications through their Part D plan. Covered Medications Eligible beneficiaries may have access to: • Foundayo (oral tablet) • Wegovy (injection and tablet formulations) • Zepbound (KwikPen only) These medications must be prescribed specifically for weight loss and long-term weight management. Eligible Medicare Plans The program is available to beneficiaries enrolled in: • Stand-alone Medicare Part D plans • Medicare Advantage plans that include Part D drug coverage • Special Needs Plans (SNPs) • Dual-eligible beneficiaries enrolled in qualifying plans Clinical Eligibility Requirements To qualify, beneficiaries must meet one of the following criteria: BMI of 35 or higher OR BMI of 30 or higher and have at least one weight-related condition, such as: • Heart failure • Uncontrolled hypertension • Chronic kidney disease (Stage 3a or higher) OR BMI of 27 or higher and have at least one of the following: • Prediabetes (based on American Diabetes Association guidelines) • Previous heart attack • Previous stroke • Symptomatic peripheral artery disease Individuals with a BMI below 27 are not eligible for the program. How to Apply Your healthcare provider must submit a prior authorization request through the program's clearinghouse before medication can be approved. Important Limitations The GLP-1 Bridge Program serves as the primary payer and does not coordinate benefits with Medicare Part D plans. You may not qualify if you have: • Type 2 diabetes • Cardiovascular disease when the medication is prescribed to treat that condition • Moderate-to-severe sleep apnea • Metabolic dysfunction-associated steatohepatitis (MASH) with moderate-to-advanced liver fibrosis For official Medicare information, visit Medicare.gov or CMS.gov . If you have questions about your Medicare coverage or prescription drug options, contact our office and we'll be happy to help. 👉 Schedule a Consultation

Long-Term Care and Its Impact on Families Most families don’t spend much time thinking about long-term care—until a health crisis suddenly changes everything. What would happen if you or a loved one developed a serious medical condition, suffered a stroke, experienced memory loss, or became unable to safely live alone? Would a family member step in as a caregiver? Could they afford to reduce work hours, absorb extra expenses, and handle the emotional strain? These are difficult questions, but they are important ones. Planning ahead can help protect your family, finances, and peace of mind. One of the most effective tools available is long-term care insurance. 👉 Learn more about retirement protection here: Retirement Planning Why More Families Need Long-Term Care Planning People are living longer than ever before, and with longer life expectancy often comes a greater need for assistance later in life. Many individuals eventually need help with activities such as: Bathing Dressing Mobility Meal preparation Medication reminders Transportation Memory-related supervision According to the U.S. Department of Health and Human Services, many adults turning age 65 today will need some form of long-term services or support during their lifetime. Official resource: https://acl.gov/ltc This is why planning ahead matters. The Emotional and Financial Impact on Families When no plan is in place, long-term care often falls on spouses, adult children, or close relatives. That can create stress in several ways: Financial Pressure Family caregivers may face: Lost wages from reduced work hours Out-of-pocket caregiving costs Home modification expenses Transportation costs Paying for outside help Emotional Pressure Caregiving can also create: Burnout Anxiety Relationship strain Less time with children or spouses Difficult decisions during already stressful times Planning early can help reduce this burden. What Long-Term Care Insurance Can Help Cover Each policy is different, but many long-term care insurance plans may help pay for services such as: In-home caregiving assistance Adult day programs Respite care Assisted living facilities Skilled nursing care Memory care / dementia care Hospice support 👉 Learn more here: Long-Term Care Insurance Aging in Place: Staying in the Home You Love Many people prefer to remain in their own home as they age. Long-term care coverage may help make that possible by covering in-home services such as: Help with bathing and dressing Meal preparation Light housekeeping Medication reminders Mobility assistance Skilled nursing visits Therapy services For many families, receiving care at home can preserve independence, comfort, and familiar surroundings. Additional Benefits Some Policies May Include Depending on the policy, long-term care insurance may also help with: Caregiver training for family members Home safety modifications Wheelchair ramps Grab bars Specialized equipment Because every policy is different, it’s important to compare benefits carefully. Why Starting Earlier Can Matter Long-term care insurance is often more affordable when purchased earlier and while in good health. Waiting may lead to: Higher premiums Fewer available options Health underwriting challenges Increased risk of needing care before coverage is in place Planning before a crisis can preserve more flexibility and control. Protecting Retirement Savings and Family Legacy Long-term care costs can be substantial. Without a plan, families may need to draw heavily from: Retirement accounts Savings Investments Home equity Coverage can help protect: Retirement income plans Assets accumulated over decades Spousal financial security Children’s inheritance goals 👉 Learn more here: Annuities Long-Term Care vs Medicare A common misconception is that Medicare covers long-term custodial care. In most cases, Medicare may cover limited skilled nursing or rehabilitation under certain conditions, but it generally does not cover ongoing custodial long-term care such as assistance with bathing, dressing, or extended nursing home stays. Official Medicare resource: https://www.medicare.gov/coverage/long-term-care 👉 Learn more here: What Is Original Medicare? Questions Every Family Should Discuss It can be helpful to talk with loved ones about: Who would provide care if needed? Would care happen at home or in a facility? How would it be paid for? Would a spouse be financially secure? How can children avoid becoming overwhelmed caregivers? Having these conversations early can prevent rushed decisions later. The Takeaway Long-term care insurance is not just about paying bills—it is about protecting dignity, independence, and family relationships. It can help reduce emotional stress, preserve retirement savings, and improve quality of life by creating options when care is needed. Rather than leaving your family with uncertainty, planning ahead gives everyone more confidence and peace of mind. Get Help Exploring Long-Term Care Options Every family’s situation is different. The right strategy depends on age, health, finances, and retirement goals. As an independent advisor, I help individuals and families review long-term care options and understand how they may fit into a broader retirement plan. 👉 Schedule a Consultation

Retiring at 62? Here Are Your Health Insurance Options Before Medicare Retiring at 62 sounds great — more time for travel, family, and enjoying life. But there’s one big question that stops many people from retiring early: What about health insurance before Medicare at 65? If you're planning to retire before Medicare eligibility, you have several options to cover the 3-year gap between age 62 and 65. Let’s walk through the most common strategies. 1. COBRA Coverage COBRA allows you to keep your employer’s health insurance after leaving your job. Pros Keep the same doctor network Same plan benefits No new deductible reset Cons You pay the full premium Coverage usually lasts 18 months Often very expensive You can learn more about COBRA coverage directly from the 👉 https://www.dol.gov/general/topic/health-plans/cobra For many retirees, COBRA is only a short-term solution. 2. ACA Marketplace Plans (Healthcare.gov) Marketplace plans through the Affordable Care Act are one of the most popular options for early retirees. Many people retiring at 62 qualify for significant premium subsidies based on income. Advantages ✔ Income-based subsidies ✔ Guaranteed acceptance ✔ Preventive care coverage Potential Downsides Narrower doctor networks PPO options are limited in some states Still, this is often the most affordable option. 3. Private Nationwide PPO Plans Some retirees prefer private PPO plans because they offer: larger doctor networks more flexibility nationwide coverage These plans can work well for people who: travel frequently want broader provider access do not qualify for ACA subsidies 4. Short-Term Health Insurance Short-term plans can provide temporary coverage while transitioning to another plan. However, they may include: limited benefits underwriting exclusions for pre-existing conditions Because of this, they are usually not the best long-term solution for retirees. 5. Health Sharing Programs Some early retirees explore health sharing ministries. While they may offer lower monthly costs, they are not traditional insurance, and coverage can vary significantly. It's important to understand the risks before choosing this option. Planning the Transition to Medicare No matter which option you choose, the goal is to bridge the gap until Medicare begins at age 65. At that point, you’ll transition into: Medicare Part A Medicare Part B A Medicare Supplement or Advantage plan A prescription drug plan Planning ahead can make that transition much smoother and less stressful. How Much Does Health Insurance Cost at 62? Costs vary depending on: household income location coverage level subsidy eligibility Some retirees pay under $200 per month with ACA subsidies, while others may pay $700–$1,200 per month for private coverage. Working with an advisor can help you compare options and avoid overpaying. Need Help Choosing the Right Plan? If you’re planning to retire before Medicare, it’s important to understand all your health insurance options. I help early retirees compare: COBRA ACA marketplace plans private PPO options strategies to bridge the gap to Medicare Related Resources You may also find these guides helpful: • What Happens If You Retire Before 65 https://www.thehealthinsuranceguy.com/retire-before-65 • Retiring Early Healthcare Costs https://www.thehealthinsuranceguy.com/retiring-early-healthcare-costs • Plan G vs Plan N Medicare Supplement Comparison https://www.thehealthinsuranceguy.com/plan-g-vs-plan-n 👉 Schedule a Consultation

What Happens If You Retire Before 65? (Health Insurance, Costs & What to Do Next) Retiring before age 65 can give you more freedom, time, and flexibility—but it also creates one major challenge: 👉 You lose employer health insurance before Medicare begins If you don’t plan ahead, this gap can cost thousands of dollars per year or force you to delay retirement altogether. The good news? With the right strategy, you can bridge the gap smoothly and affordably. If you’re thinking about retiring early, start here: 👉 Retiring Early and Bridging the Gap to Medicare What Actually Happens When You Retire Before 65 When you leave your job before 65, several things happen immediately: 1. You lose employer-sponsored health insurance Most employer plans end the last day of the month you stop working. 2. You’re not eligible for Medicare yet Medicare eligibility typically begins at age 65. 👉 That leaves a coverage gap you must fill on your own Your 3 Main Health Insurance Options Most early retirees choose between three options: 1. COBRA (Continue Your Employer Plan) COBRA allows you to keep your current employer coverage for a limited time. Pros: ✔ Same doctors and benefits ✔ No disruption in care ✔ Deductible may carry over Cons: ❌ You pay 100% of the premium ❌ Often costs $900–$1,200/month ❌ Limited to 18 months Learn more about COBRA here: https://www.dol.gov/general/topic/health-plans/cobra 2. ACA Marketplace Plans (Obamacare) ACA plans are available through the federal or state Marketplace and often include income-based subsidies. Pros: ✔ Lower premiums (if you qualify) ✔ Multiple plan options ✔ Renewable each year Cons: ❌ Network restrictions (HMO/EPO common) ❌ Deductibles reset ❌ Costs depend on income 👉 Individual & Family Health Insurance 3. Private Health Insurance Private plans are purchased outside the ACA Marketplace. Pros: ✔ Broader networks (often PPO) ✔ Lower cost for healthy individuals ✔ Flexible plan designs Cons: ❌ Health approval may be required ❌ No ACA subsidies 👉 These can be a strong option if you are healthy and don’t qualify for subsidies. The Biggest Financial Risk (Most People Miss This) Health insurance costs aren’t just about premiums. They affect: Your retirement budget Your withdrawal strategy Your tax situation (ACA subsidies are income-based) 👉 Choosing the wrong plan can impact your entire retirement plan. The Smart Strategy for Early Retirees Instead of guessing, you should build a Retirement Health Insurance Strategy. This includes: 1. Compare all options COBRA vs ACA vs Private 2. Optimize income for ACA subsidies Small income adjustments can save thousands. 3. Match your doctors and prescriptions Don’t assume your providers are covered. 4. Plan your Medicare transition Your goal is a smooth transition at age 65. Learn more about your Medicare options here: 👉 Medicare Supplement Plans 5 Costly Mistakes to Avoid Automatically choosing COBRA Missing ACA subsidy opportunities Not checking provider networks Ignoring private plan options Waiting too long to plan When Should You Start Planning? Ideally: 👉 6–12 months before retiring This gives you time to: evaluate options adjust income avoid rushed decisions Final Thoughts Retiring before 65 is absolutely achievable—but only if you plan for health insurance correctly. The right strategy can: ✔ Save you thousands per year ✔ Reduce financial stress ✔ Help you retire sooner ✔ Set you up for Medicare success Need Help With Your Plan? We help you: Compare COBRA, ACA, and private plans Maximize savings Build a personalized retirement health insurance strategy 👉 Schedule a Consultation

What Happens If You Retire Before 65? (Health Insurance, Costs & What to Do Next) Retiring before age 65 can give you more freedom, time, and flexibility—but it also creates one major challenge: 👉 You lose employer health insurance before Medicare begins If you don’t plan ahead, this gap can cost thousands of dollars per year or force you to delay retirement altogether. The good news? With the right strategy, you can bridge the gap smoothly and affordably. If you’re thinking about retiring early, start here: 👉 Retiring Early and Bridging the Gap to Medicare What Actually Happens When You Retire Before 65 When you leave your job before 65, several things happen immediately: 1. You lose employer-sponsored health insurance Most employer plans end the last day of the month you stop working. 2. You’re not eligible for Medicare yet Medicare eligibility typically begins at age 65. 👉 That leaves a coverage gap you must fill on your own Your 3 Main Health Insurance Options Most early retirees choose between three options: 1. COBRA (Continue Your Employer Plan) COBRA allows you to keep your current employer coverage for a limited time. Pros: ✔ Same doctors and benefits ✔ No disruption in care ✔ Deductible may carry over Cons: ❌ You pay 100% of the premium ❌ Often costs $900–$1,200/month ❌ Limited to 18 months Learn more about COBRA here: https://www.dol.gov/general/topic/health-plans/cobra 2. ACA Marketplace Plans (Obamacare) ACA plans are available through the federal or state Marketplace and often include income-based subsidies. Pros: ✔ Lower premiums (if you qualify) ✔ Multiple plan options ✔ Renewable each year Cons: ❌ Network restrictions (HMO/EPO common) ❌ Deductibles reset ❌ Costs depend on income 👉 Individual & Family Health Insurance 3. Private Health Insurance Private plans are purchased outside the ACA Marketplace. Pros: ✔ Broader networks (often PPO) ✔ Lower cost for healthy individuals ✔ Flexible plan designs Cons: ❌ Health approval may be required ❌ No ACA subsidies 👉 These can be a strong option if you are healthy and don’t qualify for subsidies. The Biggest Financial Risk (Most People Miss This) Health insurance costs aren’t just about premiums. They affect: Your retirement budget Your withdrawal strategy Your tax situation (ACA subsidies are income-based) 👉 Choosing the wrong plan can impact your entire retirement plan. The Smart Strategy for Early Retirees Instead of guessing, you should build a Retirement Health Insurance Strategy. This includes: 1. Compare all options COBRA vs ACA vs Private 2. Optimize income for ACA subsidies Small income adjustments can save thousands. 3. Match your doctors and prescriptions Don’t assume your providers are covered. 4. Plan your Medicare transition Your goal is a smooth transition at age 65. Learn more about your Medicare options here: 👉 Medicare Supplement Plans 5 Costly Mistakes to Avoid Automatically choosing COBRA Missing ACA subsidy opportunities Not checking provider networks Ignoring private plan options Waiting too long to plan When Should You Start Planning? Ideally: 👉 6–12 months before retiring This gives you time to: evaluate options adjust income avoid rushed decisions Final Thoughts Retiring before 65 is absolutely achievable—but only if you plan for health insurance correctly. The right strategy can: ✔ Save you thousands per year ✔ Reduce financial stress ✔ Help you retire sooner ✔ Set you up for Medicare success Need Help With Your Plan? We help you: Compare COBRA, ACA, and private plans Maximize savings Build a personalized retirement health insurance strategy 👉 Schedule a Consultation

COBRA vs Marketplace Health Insurance: Which Is Better If You Lose Job Coverage? Losing employer health insurance can feel overwhelming, especially if you are not yet eligible for Medicare. Many people retiring early or leaving a job suddenly need to replace their coverage quickly. Most people assume there are only two choices: COBRA continuation cove rage ACA Marketplace plans However, there is also a third option that many people overlook: Private health insurance plans Each option has advantages depending on your income, health needs, and how long you need coverage. If you are retiring early, you may also want to read our guide on 👉 Retiring Early and Bridging the Gap to Medicare Option 1: COBRA Continuation Coverage COBRA allows you to keep the same employer health plan after leaving your job. Instead of losing coverage immediately, you can continue your existing plan for a limited time. Typical COBRA duration: 18 months after job loss Up to 36 months in certain situations The biggest advantage is that your coverage does not change. You keep: The same doctors The same provider network The same prescription coverage Learn more about COBRA rules here: https://www.dol.gov/general/topic/health-plans/cobra Pros of COBRA Keep the same doctors and hospitals Your plan remains identical to the employer plan you had before leaving your job. Deductible may carry over If you already paid a large portion of your deductible for the year, COBRA allows you to keep that progress. Cons of COBRA Higher monthly premiums When you had employer coverage, your employer likely paid a large portion of the premium. With COBRA, you must pay: 100% of the premium plus a 2% administrative fee Many people are surprised by the true cost. Example: Coverage Type Monthly Cost Employee share while working $250 COBRA full premium $750 – $1,200 Option 2: ACA Marketplace Plans The Affordable Care Act Marketplace allows individuals and families to purchase private health insurance plans. These are commonly called ACA or Obamacare plans. Many households qualify for premium tax credits, which can dramatically reduce monthly premiums. You can explore plans here: https://www.healthcare.gov You can also learn more about individual coverage options on our page: 👉 Individual & Family Health Insurance Pros of Marketplace Plans Income-based subsidies Depending on income, many households receive subsidies that lower monthly premiums. Learn about ACA savings here: https://www.healthcare.gov/lower-costs/ Multiple plan options Marketplace plans typically offer: Bronze plans (lower premiums) Silver plans Gold plans (lower out-of-pocket costs) Cons of Marketplace Plans Provider networks may change Many ACA plans use HMO or limited networks, meaning your current doctors may not participate. Deductibles usually reset Switching to a marketplace plan typically means starting a new deductible, even if you already paid toward one under your employer plan earlier in the year. Option 3: Private Health Insurance (Off-Marketplace) Another option is private health insurance purchased outside the ACA marketplace. These plans are offered directly by insurance companies or through licensed brokers. Private plans may include: Nationwide PPO plans Underwritten health plans Association plans Short-term health insurance These options are often useful for healthy individuals who do not qualify for ACA subsidies. Pros of Private Health Insurance Nationwide PPO networks Many private plans offer broader networks than ACA marketplace plans. This can allow you to keep your doctors without being restricted to a local HMO network. Lower premiums for healthy applicants Private plans sometimes cost less than COBRA or ACA plans for people in good health. Flexible plan designs Private plans may offer more flexibility with: Deductible levels Copays Out-of-pocket limits Cons of Private Plans Medical underwriting may apply Some private plans require health questions and may not accept applicants with certain medical conditions. Not eligible for ACA subsidies Unlike marketplace plans, private coverage does not qualify for income-based premium tax credits. COBRA vs Marketplace vs Private Plans Feature COBRA Marketplace Private Plans Coverage Same employer plan ACA-compliant plan Private carrier plans Premium Usually highest Lower with subsidies Often moderate Doctors Same network May change Often broader PPO Deductible Continues Usually resets New deductible Duration 18 months Renewable yearly Depends on plan Underwriting No No Sometimes When COBRA Makes Sense COBRA may be the best option if: You are in the middle of medical treatment You already met most of your annual deductible You want to keep your exact doctors You only need coverage for a short time When Marketplace Plans Make Sense Marketplace plans often work best when: You qualify for premium subsidies COBRA premiums are too expensive You need coverage for several years You are retiring early before Medicare Marketplace plans are commonly used as a bridge until Medicare eligibility at age 65. You can learn more about Medicare planning here: 👉 Medicare Supplement Plans When Private Plans Make Sense Private health insurance may be a good option if: You are healthy You want a nationwide PPO network You do not qualify for ACA subsidies You want an alternative to expensive COBRA coverage Many early retirees use private coverage as a temporary bridge to Medicare. Special Enrollment Period Losing employer coverage triggers a 60-day Special Enrollment Period. During this time you can enroll in: COBRA ACA Marketplace plans Private health insurance plans More information about qualifying life events: https://www.healthcare.gov/glossary/qualifying-life-event/ Final Thoughts When replacing employer health insurance, it’s important to compare all three options: COBRA continuation coverage ACA Marketplace plans Private health insurance options Each option has advantages depending on your: Income Health needs Doctors Length of coverage needed Comparing these options side-by-side can help you find the most affordable and appropriate coverage for your situation. 👉 Schedule a Consultation

Medicare Advantage Pros and Cons Medicare Advantage plans—also called Medicare Part C—are an alternative way to receive Medicare benefits through private insurance companies approved by Medicare. These plans combine Part A (hospital insurance) and Part B (medical insurance) and often include prescription drug coverage (Part D) along with additional benefits. For many retirees, Medicare Advantage plans can be attractive because they offer bundled coverage and sometimes lower premiums. However, they also come with trade-offs such as provider networks and cost-sharing for services. If you are approaching age 65 or reviewing your Medicare options, understanding the advantages and disadvantages of these plans can help you make a more informed decision. What Is Medicare Advantage? A Medicare Advantage plan is a Medicare-approved private insurance plan that replaces Original Medicare as your primary coverage. These plans must cover everything that Original Medicare covers, but they often include additional benefits not available through Original Medicare. Many Medicare Advantage plans may include benefits such as: Prescription drug coverage Dental care Vision benefits Hearing coverage Fitness programs Transportation assistance These extra benefits are a major reason many seniors choose Medicare Advantage plans. 👉 Learn more about Medicare basics here: What Is Original Medicare? Official Medicare resource: https://www.medicare.gov Pros of Medicare Advantage Medicare Advantage plans offer several potential benefits that appeal to many beneficiaries. Lower Monthly Premiums Many plans have low or even $0 monthly premiums, making them attractive for people who want lower upfront costs. All-in-One Coverage Medicare Advantage plans combine hospital, medical, and often prescription drug coverage into one single plan, which simplifies managing coverage. Extra Benefits Unlike Original Medicare, many Medicare Advantage plans include benefits such as: Dental coverage Vision exams and glasses Hearing aids Fitness memberships Original Medicare generally does not cover these services. Out-of-Pocket Maximum Protection Medicare Advantage plans include an annual out-of-pocket spending limit, which protects beneficiaries from unlimited medical expenses. Cons of Medicare Advantage Although Medicare Advantage plans offer appealing benefits, they also have some limitations to consider. Provider Networks Most Medicare Advantage plans use HMO or PPO networks, which means you may need to use specific doctors and hospitals within the network. Copays for Service Instead of predictable premiums, Medicare Advantage plans often require copays or coinsurance when you receive medical care. Prior Authorization Requirements Some services may require approval from the insurance company before treatment, which can delay care in certain situations. Plan Changes Each Year Medicare Advantage plans are renewed annually, and benefits, provider networks, and drug coverage may change each year. Who Should Consider Medicare Advantage? Medicare Advantage plans may be a good fit for people who: Want lower monthly premiums Prefer all-in-one coverage Are comfortable using provider networks Want access to extra benefits like dental or vision However, people who travel frequently or want complete flexibility with doctors may prefer Medicare Supplement plans instead. 👉 Learn more here: What Are Medicare Supplement Plans? When Can You Enroll in Medicare Advantage? You can enroll in a Medicare Advantage plan during several enrollment periods: Initial Enrollment Period when you first become eligible for Medicare Annual Election Period (Oct 15 – Dec 7) each year Medicare Advantage Open Enrollment (Jan 1 – Mar 31) During these periods, you may be able to switch plans or enroll for the first time. Official enrollment details: https://www.medicare.gov/plan-compare Get Help Choosing the Right Medicare Plan Choosing between Medicare Advantage, Medicare Supplement, and Original Medicare can be confusing. The right plan depends on your healthcare needs, budget, and long-term goals. As an independent advisor, I help individuals compare Medicare plans from multiple insurance companies so they can find coverage that fits their needs. There is no cost for my guidance, and I can help you understand your options. 👉 Schedule a Consultation

Plan G vs Plan N: Which Medicare Supplement Plan Is Better? When enrolling in Medicare, many people compare Medicare Supplement Plan G vs Plan N. These two Medigap plans are among the most popular options available because they help cover the out-of-pocket costs that Original Medicare does not pay. Both plans work alongside Original Medicare (Part A and Part B) and provide nationwide access to doctors who accept Medicare. However, there are some important differences between the two plans that may influence which one is right for you. 👉 Learn more about Medicare basics here: What Is Original Medicare? Official Medicare resource: https://www.medicare.gov What Is a Medicare Supplement Plan? Medicare Supplement plans, also known as Medigap, help pay some of the healthcare costs left over after Medicare pays its portion. Original Medicare typically pays about 80% of approved medical costs, leaving beneficiaries responsible for the remaining 20%, along with deductibles and coinsurance. Medigap plans help reduce those out-of-pocket costs. 👉 Learn more here: What Are Medicare Supplement Plans? Official Medicare resource: https://www.medicare.gov/supplements-other-insurance/medigap What Plan G Covers Medicare Supplement Plan G is one of the most comprehensive Medigap plans available. Once you pay the Medicare Part B deductible, Plan G covers nearly all remaining Medicare-approved expenses. Plan G typically covers: Part A hospital coinsurance Part A deductible Part B coinsurance Skilled nursing facility coinsurance Hospice coinsurance Part B excess charges Foreign travel emergency coverage 👉 Learn more here: What Is Medicare Supplement Plan G? What Plan N Covers Plan N provides similar coverage to Plan G but with a few cost-sharing differences. Plan N typically includes: Part A hospital coinsurance Part A deductible Skilled nursing facility coinsurance Hospice coinsurance Foreign travel emergency coverage However, Plan N requires: Up to $20 copay for doctor visits Up to $50 copay for emergency room visits Payment of Part B excess charges in certain situations Because of these cost-sharing features, Plan N generally has lower monthly premiums than Plan G. What Are Part B Excess Charges? One important difference between Plan G and Plan N is coverage for Part B excess charges. Some doctors are allowed to charge up to 15% more than the Medicare-approved amount for services. Plan G covers these excess charges Plan N does not More information from Medicare: https://www.medicare.gov/basics/costs/medicare-costs/provider-acceptance Which Plan Is Better? The best plan depends on your healthcare usage and financial preferences. Plan G May Be Better If You: Want predictable healthcare costs Prefer minimal out-of-pocket expenses Want protection from excess charges Expect frequent doctor visits Plan N May Be Better If You: Want lower monthly premiums Are comfortable paying occasional copays Visit doctors less frequently Live in an area where excess charges are uncommon Plan G vs Plan N vs Medicare Advantage Some people also compare these plans with Medicare Advantage plans, which work differently than Medigap. Feature Plan G / Plan N Medicare Advantage Works With Original Medicare Replaces Original Medicare Provider Networks None Usually required Copays Limited Common Travel Flexibility Nationwide Often regional Extra Benefits Usually none Dental, vision, hearing often included 👉 Learn more here: Medicare Advantage vs Medicare Supplement When Can You Enroll in Plan G or Plan N? The best time to enroll in a Medicare Supplement plan is during your Medigap Open Enrollment Period. This period begins when: You are 65 or older, and You are enrolled in Medicare Part B During this time: Insurance companies cannot deny coverage No medical underwriting is required All plans are available Official Medicare information: https://www.medicare.gov/health-drug-plans/medigap Get Help Comparing Medicare Plans Choosing the right Medicare Supplement plan depends on your health needs, budget, and long-term preferences. As an independent advisor, I help individuals compare Medicare Supplement plans from multiple insurance companies and understand the differences between Plan G, Plan N, and other options. There is no cost for my assistance, and I can help you determine which plan may be best for your situation. 👉 Schedule a Consultation

What Is Medicare Supplement Plan G? Choosing the right Medicare coverage is one of the most important decisions people face when they turn 65. One option that has become increasingly popular in recent years is Medicare Supplement Plan G. Plan G is a Medigap plan designed to help cover many of the out-of-pocket costs left behind by Original Medicare. For many retirees, it offers predictable healthcare costs and the flexibility to see doctors nationwide. In this guide, we’ll explain how Plan G works, what it covers, and who it may be best for. What Is a Medicare Supplement Plan? Before understanding Plan G, it helps to understand how Medicare Supplement (Medigap) plans work. Original Medicare includes: Part A – hospital coverage Part B – doctor and outpatient services However, Medicare typically only pays about 80% of approved medical costs, leaving you responsible for deductibles, copays, and coinsurance. Medicare Supplement plans help cover many of those remaining costs. 👉 Learn more here: What Are Medicare Supplement Plans? Official Medicare resource: https://www.medicare.gov/supplements-other-insurance/medigap What Does Medicare Plan G Cover? Plan G is one of the most comprehensive Medigap plans available today. Once you pay the Medicare Part B deductible, Plan G covers nearly all remaining Medicare-approved costs. Plan G typically covers: Medicare Part A coinsurance and hospital costs Medicare Part B coinsurance (after deductible) Skilled nursing facility coinsurance Hospice care coinsurance Part A deductible Foreign travel emergency coverage Blood transfusions (first 3 pints) The only major expense not covered is the annual Medicare Part B deductible. 👉 Learn more about Medicare costs here: https://www.medicare.gov/basics/costs What Plan G Does Not Cover Although Plan G provides extensive coverage, there are a few things it does not include. Plan G does not cover: Medicare Part B deductible Prescription drugs Dental care Vision services Hearing aids Long-term care For prescription drug coverage, you would typically enroll in a Medicare Part D plan. 👉 Learn more here: What Is Medicare Part D? Why Plan G Is So Popular Since Medicare discontinued Plan F for new beneficiaries, Plan G has become the most popular Medicare Supplement plan. Many people choose Plan G because it offers: Very predictable healthcare costs Freedom to see any doctor that accepts Medicare Nationwide coverage without networks Protection from large medical bills Because of these benefits, Plan G is often considered the closest alternative to the former Plan F. Who Should Consider Plan G? Plan G may be a good option for people who: Want predictable healthcare costs Prefer freedom to see any Medicare provider Travel frequently in the U.S. Want strong protection against large medical bills For individuals who expect frequent healthcare visits or want stability in retirement, Plan G is often a strong option. When Can You Enroll in Plan G? The best time to enroll in a Medicare Supplement plan is during your Medigap Open Enrollment Period, which begins when you turn 65 and enroll in Medicare Part B. During this period: You cannot be denied coverage No health questions are required Insurance companies must offer you a policy More information can be found here: https://www.medicare.gov/health-drug-plans/medigap Get Help Comparing Medicare Plans Medicare decisions can be confusing, especially when comparing different plan options. As an independent advisor, I help individuals review their Medicare options and compare plans from multiple insurance companies. There is no cost for my assistance, and I can help you determine whether a Medicare Supplement plan like Plan G may be right for you. 👉 Schedule a Consultation

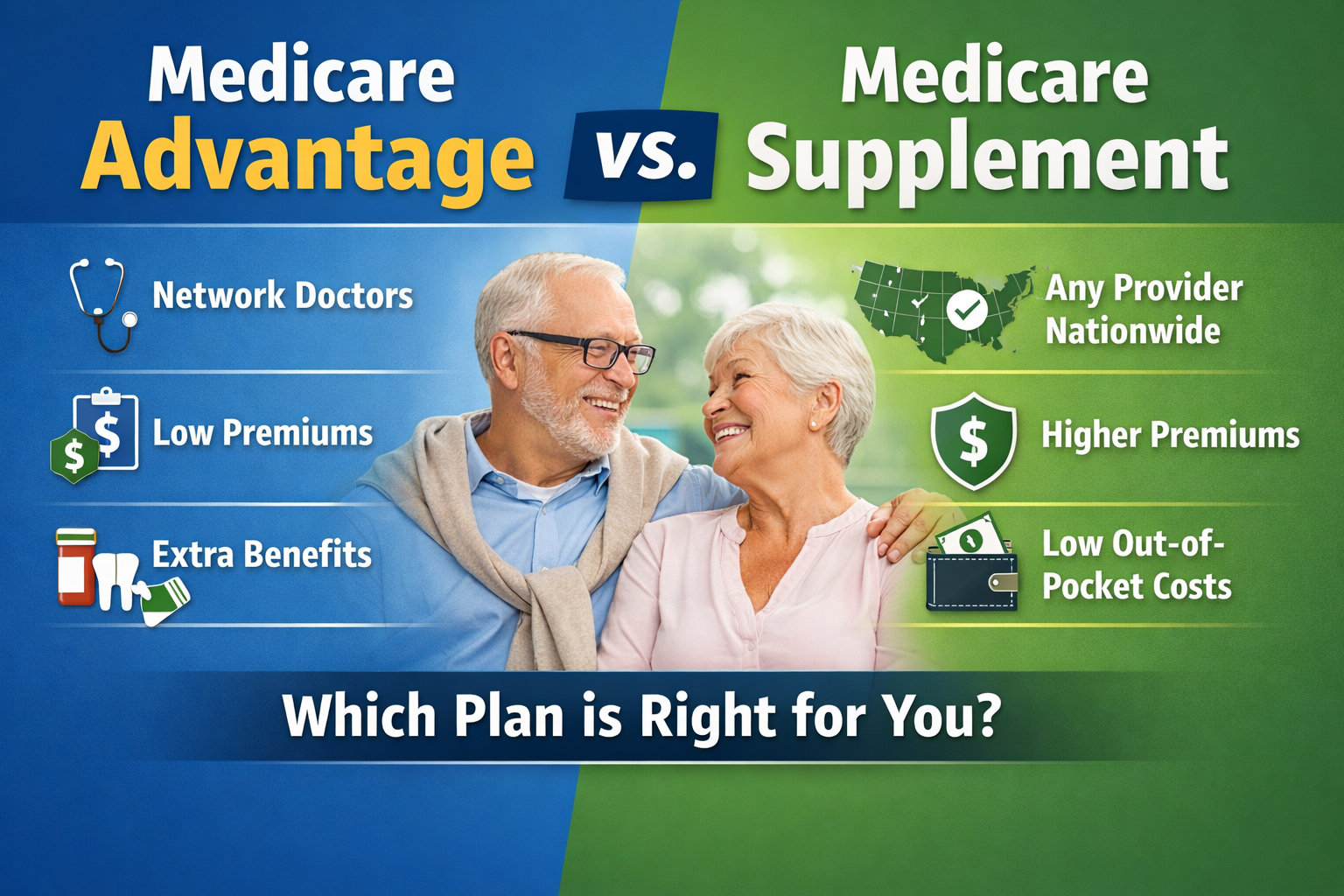

Medicare Advantage vs Medicare Supplem ent Choosing the right Medicare coverage is one of the most important decisions you’ll make when you turn 65 or become eligible for Medicare. Two of the most common options are Medicare Advantage plans and Medicare Supplement plans (Medigap). While both options help cover healthcare costs beyond Original Medicare , they work very differently. Understanding the differences can help you choose the coverage that best fits your health needs, budget, and lifestyle. 👉 Learn more about Medicare basics here: What Is Original Medicare? Official Medicare resource: https://www.medicare.gov What Is Medicare Advantage? Medicare Advantage (Part C) plans are offered by private insurance companies approved by Medicare. These plans combine Part A (hospital coverage) and Part B (medical coverage) into a single plan. Many Medicare Advantage plans also include: Prescription drug coverage (Part D) Dental benefits Vision benefits Hearing coverage Fitness programs However, most Advantage plans require members to use provider networks , such as HMOs or PPOs. 👉 Learn more here: What Are Medicare Advantage Plans? What Is Medicare Supplement (Medigap)? Medicare Supplement plans, also known as Medigap, are designed to help cover the out-of-pocket costs that Original Medicare does not pay. Original Medicare typically covers about 80% of approved medical costs , leaving beneficiaries responsible for deductibles and coinsurance. Medicare Supplement plans help pay many of those remaining costs. With a Medigap plan: Medicare pays first Your supplement pays second You may have little or no out-of-pocket costs for covered services 👉 Learn more here: What Is a Medicare Supplement Plan? Which Option Is Better? The right choice depends on your priorities and healthcare needs. Medicare Advantage May Be Better If You: Want lower monthly premiums Prefer bundled coverage including dental and vision Are comfortable using a provider network Don’t mind paying copays when you receive care Medicare Supplement May Be Better If You: Want predictable healthcare costs Prefer freedom to see any Medicare provider nationwide Travel frequently within the United States Want fewer out-of-pocket surprises Many people choose Medicare Supplement plans because they provide more predictable healthcare costs and flexibility with providers . Prescription Drug Coverage If you enroll in a Medicare Supplement plan, you will typically need a separate Medicare Part D plan for prescription drug coverage. 👉 Learn more here: What Is Medicare Part D? Medicare Advantage plans often include prescription drug coverage built into the plan. Official Medicare information: https://www.medicare.gov/drug-coverage-part-d Important Things to Consider Before choosing a plan, it’s important to evaluate: Your current doctors and provider networks Prescription medications Expected healthcare usage Monthly premium budget Long-term flexibility Every situation is different, and reviewing your options carefully can help ensure you select the coverage that fits your needs. Get Help Comparing Medicare Plans Medicare plans can be complicated, but you don’t have to navigate the process alone. As an independent advisor, I help individuals compare multiple Medicare options and understand how each plan works. There is no cost for my assistance , and I can help you evaluate both Medicare Advantage and Medicare Supplement plans. 👉 Schedule a Consultation